.png)

Your two options for covering most of the gaps that Medicare leaves behind come in the form of Medicare Advantage plans and Medicare Supplement aka Medigap plans.

Both cover these gaps in slightly different ways, so we'll go over both of them and leave you with a comparison at the end of where we think one may be stronger than the other.

Medicare Advantage

STRENGTHS & WEAKNESSES

Medicare Advantage plans replace your Government-sponsored coverage. This means that the private insurance companies that offer Medicare Advantage plans will take on all the risk and and handle all of the claims for your hospital and medical coverage. You will have 1 insurance card provided by the insurance company and you will not use your Medicare card you received from Health & Human Services (HHS).

(Do Not throw away your Medicare card. Keep it safe. You just won't need to show it while you have a Medicare Advantage plan)

The government pays these companies a monthly amount to subsidize these costs.

Strengths:

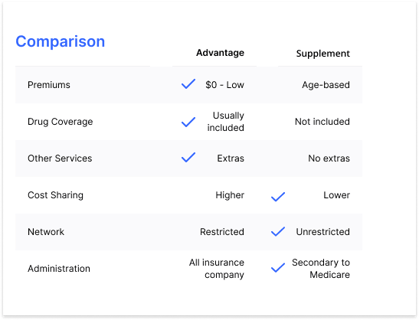

Premiums

Advantage plans have low premiums with some plans as low as $0.

Drug Coverage

Advantage plans typically include prescription drug coverage (Part D).

Other Services

Advantage plans often come with additional services like dental, vision, & hearing coverage as well as gym memberships and other perks.

Weaknesses:

Cost Sharing

You will have higher cost sharing with Advantage plans than with Supplement plans. This means you will be responsible for costs like copays and coinsurance that you wouldn’t have with Supplement plans.

Network

Advantage plans have specific provider networks connected with the insurance company or carrier you choose to work with. These networks are often strong in certain geographic areas, but weak in others.

All Benefits Through Carrier

All Advantage plan benefits are subject to the carrier’s rules, exclusions, and processes that will typically be less inclusive than a Supplement plan.

Medicare Supplement aka Medigap

STRENGTHS & WEAKNESSES

The terms Medicare Supplement and Medigap are used interchangeably and mean the same thing. Medicare Supplement plans pay secondary to traditional Medicare. This means that Medicare picks up the 80% coverage and then sends the claim and bill to the Supplement plan to cover the remaining 20%.

You will use your Medicare card provided to you by Health & Human Services (HHS) and you will carry an additional card provided to you by the insurance company you choose for your Supplement plan.

Strengths:

Cost Sharing

The most popular supplement plan (Plan G) has a $203 annual deductible. Once that is met, you have zero medical cost sharing responsibility as long as the expense is covered by Medicare.

Network

Supplement plans do not have a network. You can visit any provider, anywhere in the country as long as the provider participates with Medicare.

Secondary to Medicare

Since Supplement plans are secondary to Medicare, coverage policies, exclusions, and procedures align with Medicare, which are generally more inclusive than Advantage plans.

Weaknesses:

Premiums

Premiums are age-based, meaning the higher your age, the more expensive. Premiums start around $100 per month and go up depending on the plan you choose, the company you choose, and your age, and oftentimes your gender.

Drug Coverage

Part D prescription drug coverage is not included with Supplement plans.

Other Services

Supplement plans do not come with the same additional services as Advantage plans. Bells and whistles like dental, vision, and hearing benefits will not be included with Supplement plans.

Which is better?

I know what you're thinking.

"But each has three check marks. It looks like a tie!"

The decision about which plan suits you best is a personal decision. Even between spouses, we often see one spouse get an Advantage plan and the other spouse get a Supplement plan. The decision is highly dependent on your situation.

In general, Advantage plans suit those who are healthier, with lower healthcare costs, and who do not plan on traveling outside their state or too far from their residential zip code. They typically have low to no drug costs and no chronic conditions. They also prefer lower monthly premiums, at times $0 depending on the carrier they choose and the individual's geographic residence.

Supplement plans tend to cater to those who know that they will be utilizing the healthcare system often, know that they will travel often and don't have to worry about a network, or prefer the peace of mind knowing that all hospital and medical costs are paid for once their deductible is met.

Wrapping it up

How you plan to cover the gaps left by Medicare is arguably one of the most important Medicare decisions you'll make. We strongly recommend using an agent you trust who represents several different carriers so that you can work together with an expert and find the perfect plan for your budget, your health, and your peace of mind.

If you have someone like that in your life... use them. It does not cost you anything to use them. Your rates do not go up or down if you use them versus going directly to the insurance company themself. The difference is, an agent should know all of the intricacies of Medicare and help you avoid any mistakes.

If you don't have someone like that in your life, call us.

Senior Benefits Insurance Services

801-523-6081