Medicare Part D is a beast.

In fact, we find that there are more questions about Part D prescription drug coverage than any other Medicare-related topic. And it makes sense as to why. Prescription medication costs are rising at scary rates and Part D coverage details are all kinds of confusing with different coverage tiers and dollar amounts.

We'll do our best to straighten this up for you.

Enrolling in Part D

The Part D enrollment window follows the same timelines as enrolling in Medicare Advantage Plans. This means that you can enroll in Part D plans at specific times of your life and/or times of the year.

The Initial Enrollment Period

If you're looking to enroll in a Part D plan when you turn 65, you can enroll:

- Up to three months prior to your birthday month.

- During your birthday month, or...

- Up to three months after your birth month.

You need to be careful if you plan on enrolling during the three months after your 65th birthday, because you could have up to three additional months of waiting period before your Medicare actually kicks in.

The Special Enrollment Period

Should you choose to retire after age 65, which means outside the Initial Enrollment Period (because you were covered by a group plan), you would be considered qualified for what is called a Special Enrollment Period.

If you have a qualifying event, meaning you retired from work and are moving off your employer's (or spouse's employer) group plan, you can pick up your Part D without penalty when you enroll within the same Part B timelines. We have a whole article on these timelines here: Medicare Timelines

The General Enrollment Period

The General Enrollment Period is January 1 to March 31st of each year with coverage beginning on July 1st of that year. If you failed to enroll in Part D during your Initial Enrollment Period or your Special Enrollment Period, you would have to wait until this General Enrollment period to be able to enroll in a Part D prescription drug plan.

This is important because should you choose not to enroll in Part D when you should, and a medical emergency comes up with high drug costs, you are responsible for 100% of those costs until you are able to enroll in a plan between January 1 and March 31 of the upcoming year. This can be devastating.

We always recommend getting a Part D plan, even if all is well right now and you aren't on any medications. You never know when life will throw a curve ball and you don't want to be stuck with 100% of the costs of drugs should something happen.

Annual Election Period (AEP)

The annual election period is from October 15th - December 7th of each year. During this time, individuals who have Part D prescription drug plans may make changes to their existing plans. These changes would go into effect on January 1 of the upcoming year.

Is there a Part D penalty?

Yes, another reason to grab a Part D plan when you are first eligible is because a penalty applies when a person chooses not to enroll in a prescription drug plan during their Initial Enrollment Period or Special Enrollment Period.

This penalty is 1% of the average monthly Part D premium per month you choose not to enroll in Part D. As of this writing, the national average monthly premium is about $43.07. That means that if you put off enrolling in Part D for 24 months, you will have a 24% Part D penalty added to your regular Part D premium for the rest of your life. 24% of the $43.07 average is $10.34. You would add the $10.34 to the premium of whichever Part D plan you choose to pick up.

Part D Premiums

Part D premiums are dependent upon the insurance company you choose to use for this plan. They will set the rates. However, for high-income earners, the government adds an extra amount to Part D monthly premiums on top of the regular amount.

Here is a chart of the income levels and the added Part D surcharge: Part B & D Income Levels

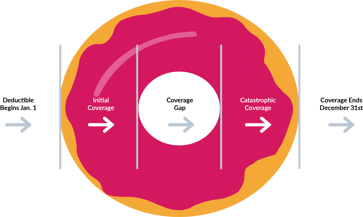

The 4 Phases of Part D Coverage

Now, let's dive into Part D prescription drug coverage. It is best to cover this by breaking it down into four separate phases, and we'll discuss each one:

-

The Deductible Phase

-

Initial Coverage

-

The Coverage Gap (The Donut Hole)

- Catastrophic Coverage

Phase 1: The Deductible Phase

The first phase of any Part D plan is the deductible phase.

Deductible dollar amounts will vary based on the plan you choose with the maximum being $445 (in 2021).

You are responsible for 100% your deductible amount before your Part D plan will start paying for any prescription drug costs. However, many plans will waive the deductible if you are only using generic medications, and this is a wonderful benefit to take advantage of.

If you're taking non-generic medications, you'll be subject to that deductible until you meet it and head into the Initial Coverage phase.

Phase 2: Initial Coverage

Once you have met your deductible, you enter the initial coverage phase. While here, you will have copays that are specific to your plan coverage.

You remain in the Initial Coverage Phase until the total cost of your deductible, your copays, and the money your plan has contributed add up to $4,130.

Phase 3: Coverage Gap

aka The Donut Hole

The coverage gap is the most notorious phase of Part D coverage because everything changes once you reach the donut hole.

While in this phase, you are responsible for 25% of the drug cost.

In Phase 2, your deductible, copays, and the amount the insurance paid all contribute to your $4,130 level to move out of that phase. To get out of the Coverage Gap, only your payments and a discount amount from drug manufacturers (usually 50% of the drug cost) are what count toward your totals.

Once the amount you’ve paid (deductible, copays, coinsurance) and the manufacturer discounts add up to $6,550, you can move into the last phase of drug coverage.

Phase 4: Catastrophic Coverage

While in the Catastrophic Coverage phase, you pay the greater of:

- 5% of the cost of the drug, or

- $9.20 per Rx for brand drugs, or

- $3.70 per Rx for generic drugs

Wrapping it up

Part D is so complex and there are several other exceptions and intricacies that just can't be covered in an article like this. We'd need to write an entire book (and we just might).

Please, don't hesitate to call us with your specific situation and we'd be happy to find out what would work best for you to help alleviate the costs of drug coverage.

Senior Benefits Insurance Services

801-523-6081